In my interaction with SME entrepreneurs, I always have this feeling that they have problems understanding the meaning of debit or credit in the context of an accounting system. This should not be the case. The reason being these terms are easy to comprehend and use. You do not need to be a student of accounting to really grasp these concepts. I believe that in the old days, the system was created as such, to make things simpler to record and to report; with a built-in internal control to ensure that all figures are processed accordingly with no missing or mistaken figure or transaction.

It is critical to understand the in-built internal control used by the system. The numbers recorded on one side will always equal to the numbers recorded on the other side.

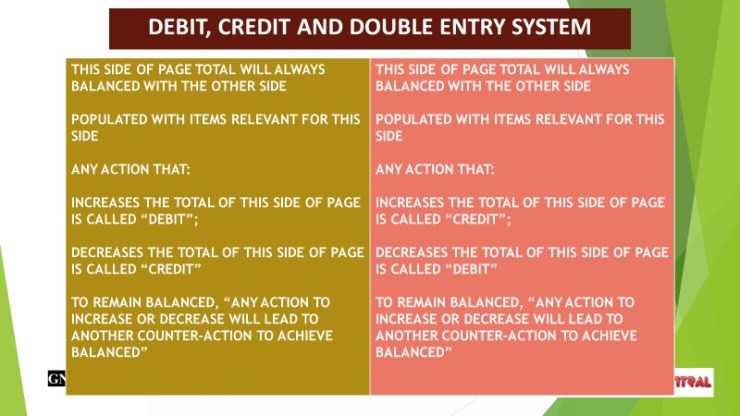

I imagine that historically the person inventing the seeds of accounting system as we know it must have taken a blank piece of paper. He then drew a vertical on the blank page to split the page into two halves. Then he proceeded to say, the left side shall be in balance with the right side all the time. An action impacting the two halves can either be an increase, a decrease or a hold.

At the start, the two halves will be balanced meaning that the Left-hand Side (LHS) amounts equals the Right-hand Side (RHS) amounts. He then invented the term “Debit” to denote actions that increase the amounts on the LHS; and “Credit” to denote actions that increase the amounts on the RHS. For the reverse actions, he proceeded to use “Credit” to denote actions that decrease the amounts on the LHS and “Debit” to denote actions that decrease the amounts on the RHS. Hence as follows:

LHS = Debits for increase in amounts; and Credits for decrease in amounts

RHS= Credits for increase in amounts; and Debits for decrease in amounts

With this, the double-entry system was created. In order to maintain the in-built internal control of a balanced LHS and RHS, any action of increase, decrease or hold would necessitate another corresponding increase, decrease or hold action.

The inventor then proceeded to populate the LHS of the page with items deemed relevant to this side, and did the same for the RHS.

When there is an increase in amount action for the LHS item, another corresponding action is performed to counter this movement, either by an increase in amount action for item in the RHS or a decrease in amount action for another item in the LHS.

Hence a debit action is counter-acted with a credit action. This is still in use until today, and remains to be known as debits and credits of the double-entry accounting system.

IN SHORT, IF THE ITEM THAT YOU ARE LOOKING AT FALLS WITHIN THE LHS, THEN ANY ACTION LEADING TO AN INCREASE IN AMOUNT IS CALLED “DEBIT”. AND VICE-VERSA.

So, what are the items that populate the LHS of the page and the RHS?

I shall explain this in my next write-up. Stay tuned!

GNZ.