In a discussion that was held recently, an issue was raised where the amount contracted with customer is to be monitored as well as the invoice issued and payment collected arising from the contract.

In the business system, the initial recording is to recognise the “Unbilled Contract Amount”. The accounting entries are as follows:

DR Customer CR Unbilled Contract Amount

The Unbilled Contract Amount is created as a Balance Sheet item to enable the tracking of amount remaining to be invoiced to the customer.

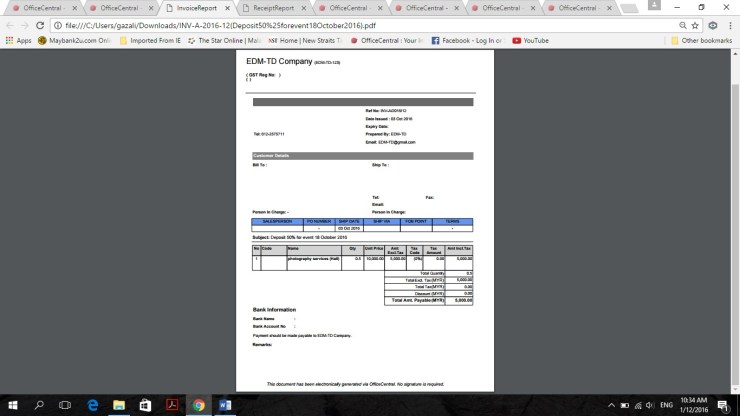

The first invoice is then issued to the customer representing a portion of the Unbilled Contract Amount. Sample of the invoice is as follows:

The accounting entries for the invoice:

DR Unbilled Contract Amount CR Sales Revenue

By this method, Sales is recognised only when the invoice issued. Not when the amount is contracted with the customer.

When the customer pays the amount as stated, a receipt is issued for the amount collected. Sample of the receipt is as follows:

The accounting entries for the receipt:

DR Bank CR Customer

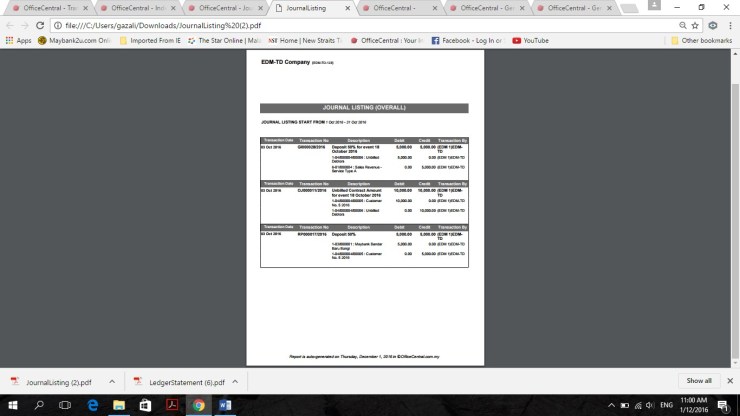

The sample of Journal Listing for the accounting transactions above is as follows:

Later on, at the required date, the second invoice is issued; and the receipt is then issued for the amount collected. The process is repeated until the Unbilled Contract Amount is exhausted and completely invoiced.

Periodically, an Account Statement can be issued to the customer to highlight the amount remaining to be invoiced and the payments made so far. Sample of Account Statement for the customer is as follows:

Note: If the transactions cross over to the next financial year, the sales recognised for the current year are the amounts invoiced. The balance carried forward as Unbilled Contract Amount represent sales when invoice is issued in the future.

GNZ.